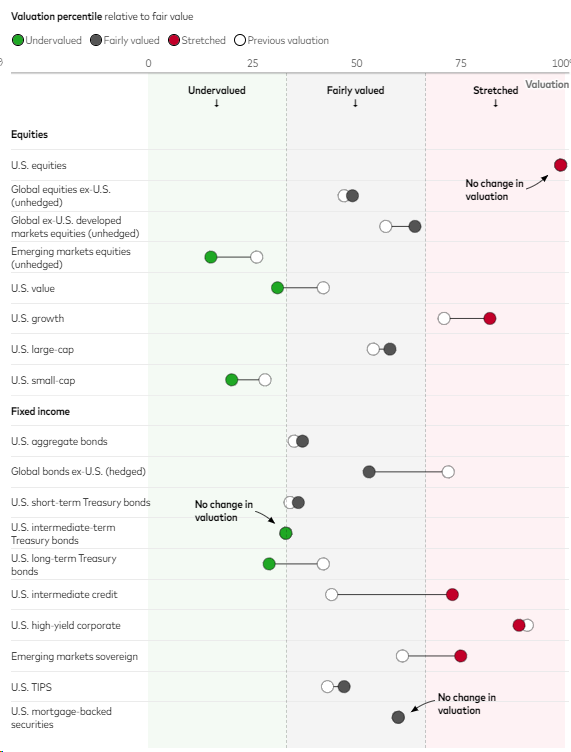

At the midpoint of 2024, the broad U.S. equity market remains richly valued. The S&P 500 Index, for example, stands about 33% above the top end of our estimated fair-value range based on its cyclically adjusted price/earnings ratio.1 The richest valuations adorn growth stocks—shares with relatively high prices in relation to their earnings and the issuing companies’ net assets. Emerging markets equities appear most undervalued.

In the bond market, we view long-term U.S. Treasuries as the most undervalued asset class. High-yield corporate debt, which carries below-investment-grade credit ratings, appears most richly valued.

To be sure, over any given investment horizon, a change in valuation is only one element of total return. For equities, the other factors are earnings growth, dividends, and the currency effects of holding international shares.

Valuations also are poor indicators of short- or even intermediate-term financial market returns. For that reason, we caution investors against adjusting well-considered investment plans based solely on valuations—no matter how strong a signal they appear to be sending.

“We focus on valuations as critical drivers of long-term market results,” said Kevin DiCiurcio, CFA, head of the Vanguard Capital Markets Model® (VCMM) research team. “We believe they have a strong tendency to revert toward average levels, consistent with prevailing inflation trends and interest rates, over multiyear periods and certainly over the course of decades. Such horizons should be relevant to many investors, given the time they may have until they reach retirement or the years they may spend in retirement.”

Potential opportunities and cautionary signals for long-term investors

Notes: The U.S. equity valuation measure is the current cyclically adjusted price/earnings ratio (CAPE) percentile relative to our fair-value CAPE estimate for the MSCI US Broad Market Index. Factor valuations are relative to U.S. equities as the base at the 50th percentile. Growth, value, and small-cap valuation measures are all based on the percentile rank based on our fair-value model relative to the market. The large-cap valuation measure is a composite valuation measure of the style factor to U.S. relative valuations and the current U.S. CAPE percentile relative to its fair-value CAPE. The emerging markets valuation measure is based on the percentile rank based on our fair-value model relative to the market. The ex-U.S. developed markets and global ex-U.S. equity valuation measures are the market-capitalization-weighted CAPE percentiles relative to our fair-value CAPE estimate for the MSCI EMU Index, MSCI UK Index, MSCI Japan Index, MSCI Canada Index, MSCI Australia Index, and MSCI Emerging Markets Index; the MSCI Emerging Markets Index is used only for global ex-U.S. equities.

Aggregate bond valuation measures are market-capitalization-weighted averages of intermediate-term credit and Treasury valuation percentiles for the U.S. and global ex-U.S. (market-capitalization-weighted averages of the euro area, the U.K., Japan, Canada, and Australia). Treasury valuation measures are the key rate duration-weighted average of our fair-value model. Intermediate credit, high-yield credit, mortgage-backed securities (MBS), and emerging markets sovereign debt valuation measures are based on current spreads relative to the VCMM simulation of spreads in year 30 of our forecast. The Treasury Inflation-Protected Securities (TIPS) valuation measure is based on the 10-year annualized inflation forecast relative to our equilibrium forecast for inflation.

The valuation percentiles are as of May 31, 2024, and December 31, 2023.

Source: Vanguard calculations using data from Robert Shiller’s website at aida.wss.yale.edu/~shiller/data.htm, the U.S. Bureau of Labor Statistics, the Federal Reserve Board, and Refinitiv, as of May 31, 2024.

IMPORTANT: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from VCMM are derived from 10,000 simulations for each modeled asset class. Simulations as of May 31, 2024, and December 31, 2023. Results from the model may vary with each use and over time. For more information, please see the Notes section below.

1 Our fair-value measure of the market’s cyclically adjusted price/earnings (CAPE) ratio starts with the CAPE metric established by Robert Shiller of Yale University. That measure reflects the last 10 years of corporate earnings, which smooths valuations based on current prices and profits. We build upon the Shiller CAPE by estimating fair values in relation to prevailing interest and inflation rates.

Notes: All investing is subject to risk, including the possible loss of the money you invest.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

U.S. government backing of Treasury or agency securities applies only to the underlying securities and does not prevent share-price fluctuations. Unlike stocks and bonds, U.S. Treasury bills are guaranteed as to the timely payment of principal and interest.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard's primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

CFA® is a registered trademark owned by CFA Institute.

Vanguard Mexico is not responsible for and does not prepare, edit, or endorse the content, advertising, products, or other materials on or available from any website owned or operated by a third party that may be linked to this email/document via hyperlink. The fact that Vanguard Mexico has provided a link to a third party's website does not constitute an implicit or explicit endorsement, authorization, sponsorship, or affiliation by Vanguard with respect to such website, its content, its owners, providers, or services. You shall use any such third-party content at your own risk and Vanguard Mexico is not liable for any loss or damage that you may suffer by using third party websites or any content, advertising, products, or other materials in connection therewith.