Commentary by: Fran Kinniry, Head of Investment Advisory Research Center, Lauren Martinelli,

Investment Strategist, Investment Advisory Research Center, Michael DiJoseph, Senior Advice Strategist Investment Advisory Research Center

Strong market performance continues despite headwinds

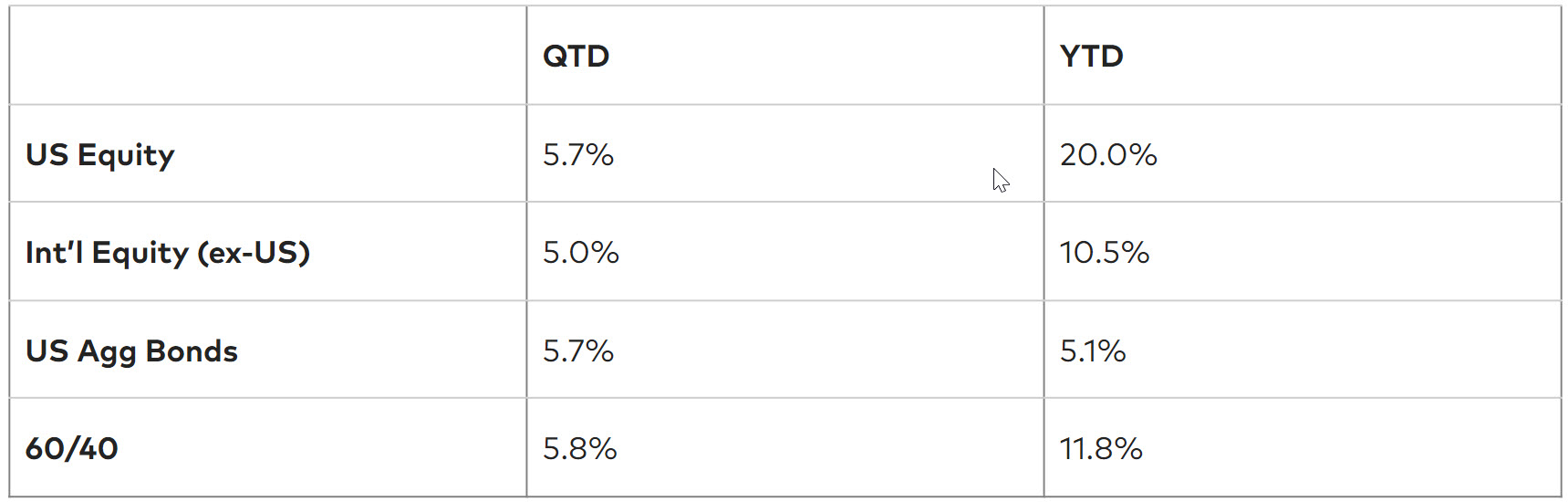

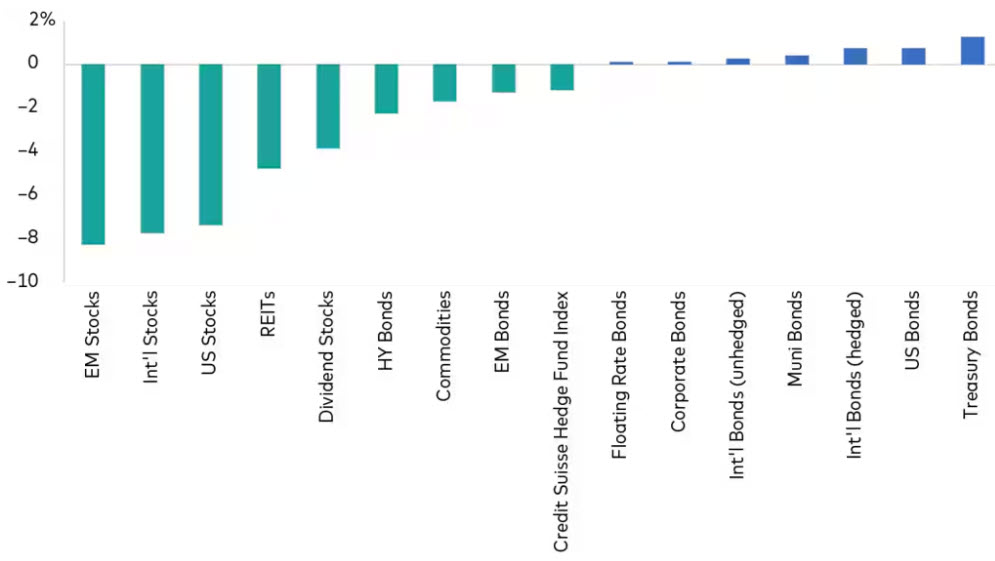

It rings true that performance over the past quarter, like much of history, has been unpredictable with bouts of volatility. Despite a handful of volatile days in the third quarter, equity markets have continued to post new all-time highs this year, with above-average quarter and year-to-date results as shown in Figure 1. Advisors that coached clients to stay the course, despite the noise, delivered value through exceptional portfolio performance.

Figure 1: Quarter and year-to-date performance (as of September 24, 2024)

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index

Source: Investment Advisory Research Center calculations using data from Morningstar. Performance figures as of September 24, 2024.

Notes: US Equity benchmark using data from CRSP Total Market Index, International Equity benchmark using data from FTSE Global All Cap ex- US, US Agg Bonds benchmark using data from Bloomberg US Aggregate Float Adjusted Index. 60/40 benchmark data allocated as follows: 36% CRSP Total Market Index, 24% FTSE Global All Cap ex-US, 28% Bloomberg US Aggregate Float Adjusted Index, and 12% Bloomberg Global Aggregate Float Adjusted Index ex US.

With above average market performance in 2024, why doesn’t it feel like it’s another banner year?

Starting in mid-July through early August, the S&P 500 experienced a cumulative drawdown of more than 10% in three short weeks. This drawdown period garnered widespread media attention and amplified the voices of permabears who once again called for the end of the long-running bull market. As the market declined, predictions of a bear market on the horizon started to grow louder. Not so fast. The market rebounded swiftly and was able to momentarily quiet the noise of financial headlines that predicted further volatility.

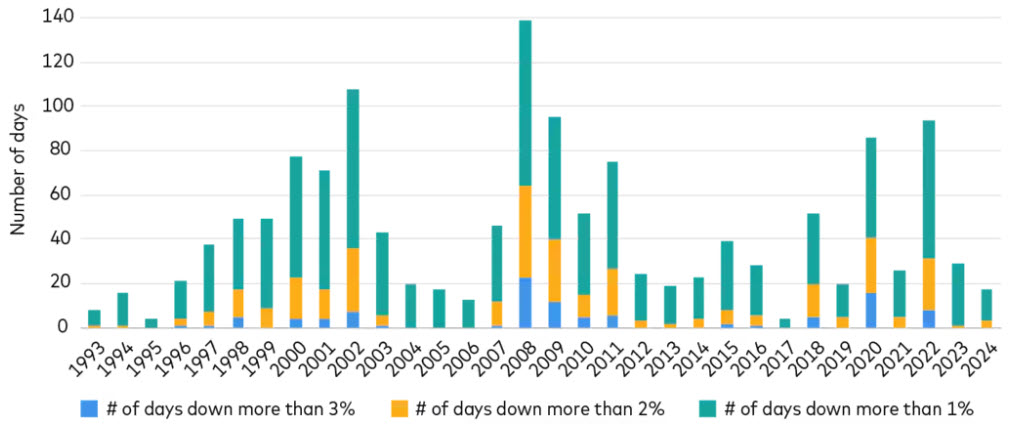

Long-term perspective reminds us that the third quarter drawdown was more closely aligned with historical market volatility than what we experienced in the first half of the year. Figure 2 illustrates that, through three quarters of the year, the S&P 500 has experienced about half the number of volatile days compared to an average year.

Because of the relatively calm start to the year, it’s possible that clients were taken aback during the stretch of negative performance. At times, headlines were bearish with markets down between 5%-10%, depending upon the index. The best advisors were prepared for this, though. Acting as a behavioral coach and helping clients stay the course during the volatility, they helped add value to portfolios and kept clients on track to meet their financial goals. This is a prime example of Advisor’s Alpha in action.

Figure 2: Number of historical 1%, 2%, 3+% drawdown days S&P 500 drawdown days by %

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Source: Investment Advisory Research Center using data from FactSet. Figures represent S&P 500 daily returns from 1928 through September 18, 2024.

With fewer volatile days thus far this year, the equity markets continue to reach, or near, new all-time highs. When markets reach all-time highs, it is common to hear predictions that call for a correction. However, Figure 3 illustrates markets have often continued their positive momentum after current period returns are positive. Again, the most important thing is to tune out the noise.

Figure 3: Markets continue upward trajectory after reaching new all-time highs

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Notes: S&P 500 daily returns from 1928 through June 2024.

Source: Investment Advisory Research Center using data from Morningstar, Inc.

Advisors are successfully rebalancing portfolios to maintain target allocations

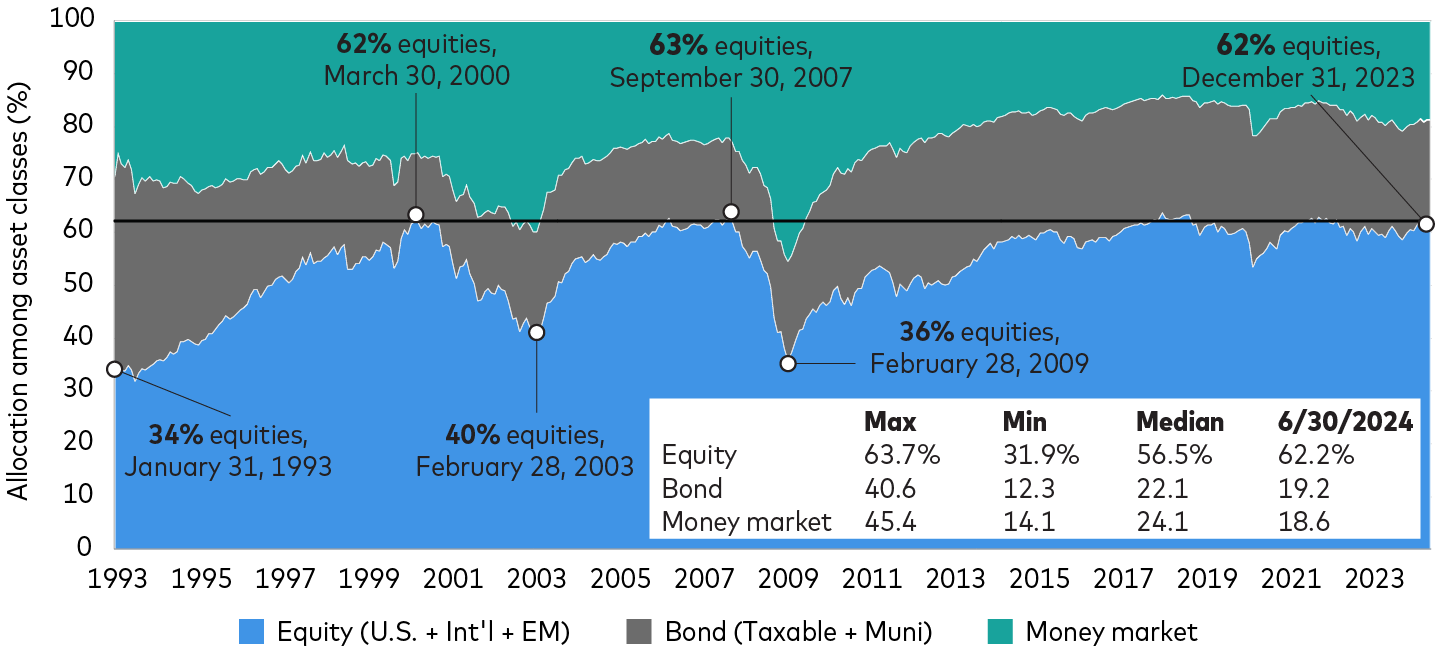

Remember, an advisor’s job is never done and staying the course does not mean standing still. While equity market success is beneficial for investors, portfolios can become susceptible to a drifting asset allocation, especially when equities have had such extreme outperformance over bonds for all recent time periods. For example, the periods of: year-to-date through September 24, 3-, 5-, and 10-year returns of stocks minus bonds have been 15%, 32%, 100%, and 209%, respectively1 . Rebalancing is equally as important during a market upswing, and over extended periods, as it is during a downturn. Though it may seem counterintuitive to rebalance while equity performance is at historical highs, failure to do so may increase a client’s risk within their portfolio. Without appropriately rebalancing, stocks can become overweighted relative to lower risk asset classes such as fixed income and can negatively impact client’s abilities to achieve their long-term financial goals.

Our Risk Speedometers demonstrate the value of rebalancing, and a job well-done by advisors, in helping investors stick to their target asset allocation. Fixed income has captured a significant portion of cash flows over the past one-, five-, and ten-year periods. Given the equity market’s upward trajectory, flows into fixed income would have significantly altered asset allocation had it not been attributable to rebalancing. We hypothesize that the relatively stable asset allocations over this same period, as seen in Figure 4, is a product of rebalancing and industry changes in the delivery of investment advice rather than a shift of investment philosophy. This is different behavior than what we saw in the late 1990s and mid 2000s: These bull markets saw flows into equities, not bonds, as investors attempted to chase positive momentum. Staying the course and rebalancing during the longest yield curve inversion in history has been no easy task for advisors, but they have done it!

Figure 4: Advisors successfully coach clients to better outcomes with disciplined rebalancing

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Sources: Vanguard Investment Advisory Research Center calculations using data from Morningstar, Inc.

Note: Black line illustrates equity allocation (62.2% as of June 30, 2024) to visualize the variance of equity allocations (blue area) through time.

Timing the markets is a challenge

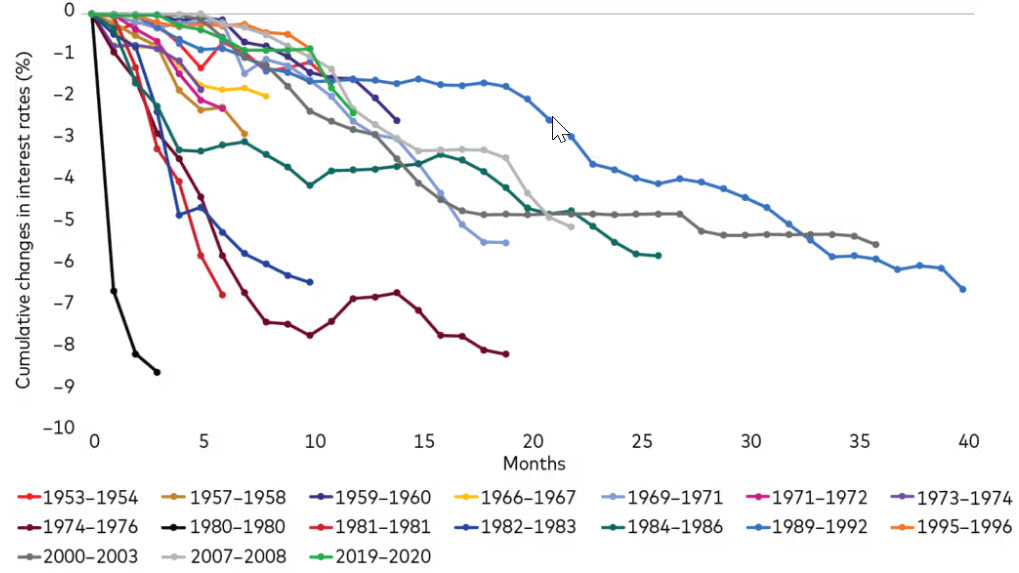

Of course, bouts of volatility were not the only notable occurrence on your clients’ minds over the third quarter. The Fed began its long-anticipated rate-cutting cycle on September 15 with a 50 bps rate cut. It was the first action taken by the Fed in approximately 14 months since a 25 bps hike in July 2023. Additionally, this was the first rate cut since March of 2020. Figure 5 illustrates that the path forward, as should be expected, is uncertain, with no two previous easing cycles being the same from a magnitude, duration, and speed perspective.

The uncertain path of rates should be a great reminder that the markets are dominated by a very large universe of professional traders and allocators of capital who set prices on assets based on forward-looking expectations. What most often causes a future market decline is when new information deviates from what professional investors have priced in as consensus. History tells us that trying to time the markets, including interest rates, has been challenging. When new information becomes available, professional traders and allocators react instantaneously. Rather than advisors trying to predict the direction of interest rates, often using stale information, these decisions can be outsourced to top-performing active fixed income managers, such as Vanguard’s Active Fixed Income Group, whose primary focus is to add fixed income alpha.

Figure 5: Predicting the path of interest rates is challenging

Magnitude of historical interest rate easing cycles from peak rates to trough

Sources: Vanguard Investment Advisory Research Center calculations using data from Morningstar and Federal Reserve Economic Data (FRED).

Fixed income serves as a ballast to equity

Regardless of the future path of rates, it’s important to remember the role of bonds in a portfolio. It’s noteworthy that fixed income has served its purpose well as a diversifier in the portfolio and an important ballast to equity markets this past quarter. The US Agg2 has continued positive monthly returns in the third quarter and outperformed cash (as represented by the Bloomberg US 3-month Treasury Bellwether Index) by more than 4% in the quarter. In a well-diversified portfolio, high-quality fixed income yields provide a cushion in the portfolio with less risk compared to equities, particularly for investors that are in or nearing retirement and may have a higher portion of their portfolio allocated to less risky assets. Figure 6 shows historical median monthly performance of fixed income during bottom decile equity returns, demonstrating the role and value of high-quality fixed income as both ballast and a diversifier in the portfolio.

Figure 6: High-quality fixed income is a good ballast to equity

Median monthly return during bottom decile U.S. equity returns (1988 through August 2024)

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Sources: Investment Advisory Research Center, calculated using Morningstar Inc., and FactSet data.

Staying the course does not mean standing still

Fourth quarter market performance, and the path of the interest rate easing cycle, remains unpredictable. As uncertainty is the common denominator regarding future market performance, we are reminded that staying the course does not mean standing still, which applies during both bull and bear markets.

It’s critical to regularly revisit a client’s goals, asset allocation, and risk tolerance. A client’s goals may change regardless of market performance, and these changes don’t always align well with the timing of market cycles. A change in goals may be caused by an addition to the family, change in employment status, or inheritance from intergenerational wealth. As you help clients anchor to their goals, rather than market performance, you can help them tune out market noise, navigate uncertainty, and remain laser focused on achieving those goals. Meanwhile, you can acknowledge that it’s been another great quarter for clients whom you’ve helped stay the course!

1 Stock benchmark represented by CRSP US Total Market Index. Bond benchmark represented by Bloomberg US Aggregate Float Adjusted Index.

2 Fixed income benchmark represented by Bloomberg US Aggregate Float Adjusted Index.

Notes:

All investing is subject to risk, including possible loss of principal.

Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Diversification does not ensure a profit or protect against a loss.

Past performance is not a guarantee of future results.

CFA® is a registered trademark owned by CFA Institute.

Data provided by Morningstar is property of Morningstar and Morningstar’s data providers and it should therefore not be copied or distributed. Morningstar and its data providers are not responsible for any certification or representation with respect to data validity, certainty, or accuracy and are therefore not responsible for any losses derived from the use of such information.

Bloomberg® and Bloomberg Indexes mentioned herein are service marks of Bloomberg Finance LP and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by Vanguard. Bloomberg is not affiliated with Vanguard and Bloomberg does not approve, endorse, review, or recommend the Financial Products included in this document. Bloomberg does not guarantee the timeliness, accurateness or completeness of any data or information related to the Financial Products included in this document.

Vanguard Mexico is not responsible for and does not prepare, edit, or endorse the content, advertising, products, or other materials on or available from any website owned or operated by a third party that may be linked to this email/document via hyperlink. The fact that Vanguard Mexico has provided a link to a third party's website does not constitute an implicit or explicit endorsement, authorization, sponsorship, or affiliation by Vanguard with respect to such website, its content, its owners, providers, or services. You shall use any such third-party content at your own risk and Vanguard Mexico is not liable for any loss or damage that you may suffer by using third party websites or any content, advertising, products, or other materials in connection therewith.